A French introduction to Sentometrics published in CScience.ca

The Sentometrics field is introduced in French in CScience.ca.

Check out the papers and the indices discussed in the article !

Ardia, D., Bluteau, K., Boudt, K., Inghelbrecht, K.

Our research featured in The New York Times and Les Affaires

Our research on climate change concerns and financial markets has been featured in The New York Times and Les Affaires.

Check out the paper on this index!

Ardia, D.

Media Abnormal Tone, Earnings Announcements, and the Stock Market

We show that media provide incremental information relative to the information contained in earnings press releases and earnings calls, and on aggregate, market participants overreact to it!

The complementary role of the news media stems from their transformation of earnings-related information into a more easily understandable, contextualized, and condensed format and the additional information it can provide given critical contemporary events.

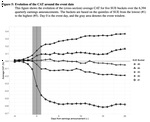

A Century of Economic Policy Uncertainty Through the French-Canadian Lens

Leveraging a historical French-Canadian newspaper data set provided by the Bibliothèque et Archives Nationales du Québec (BAnQ) as well as a research collaboration with Radio-Canada, we have developed a century-long historical Economic Policy Uncertainty (EPU) index for the Canadian province of Quebec.

Media Climate Change Concerns Index

Many consider climate change as one of the biggest challenges of our times. However, there is disagreement on the magnitude of the climate change problem and how to solve it.

Daily Topical US Economic Sentiment Indices

The added advantage of text- and news-based measures as sources of information for forecasting and assessing the economy is significant. In a recent paper of ours, we present a general methodology, which constitutes the base of the sentometrics R package, to forecast economic variables from news data.

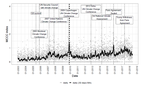

The Economic Policy Uncertainty Index for Flanders, Wallonia and Belgium

The Economic Policy Uncertainty (EPU) measures the economic risk when the government policy’s future path is uncertain. This index can detect events and trends which correlate, for instance, with economic health and stock market downturns.

The R package sentometrics

The sentometrics package offers an integrated framework for textual sentiment time series aggregation and prediction. It accounts for the intrinsic challenge that textual sentiment can be computed in many different ways, as well as the large number of possibilities to pool sentiment into a time series index.

Introducing the sentometrics field

The advent of massive amounts of textual, audio, and visual data has spurred the development of econometric methodology to transform qualitative sentiment data into quantitative sentiment variables, and to use those variables in an econometric analysis of the relationships between sentiment and other variables.